JPMorgan Cuts 2026 Average Gold Forecast — But Keeps $6,300 Year-End Target Intact

JPMorgan Cuts 2026 Average Gold Forecast — But Keeps $6,300 Year-End Target Intact

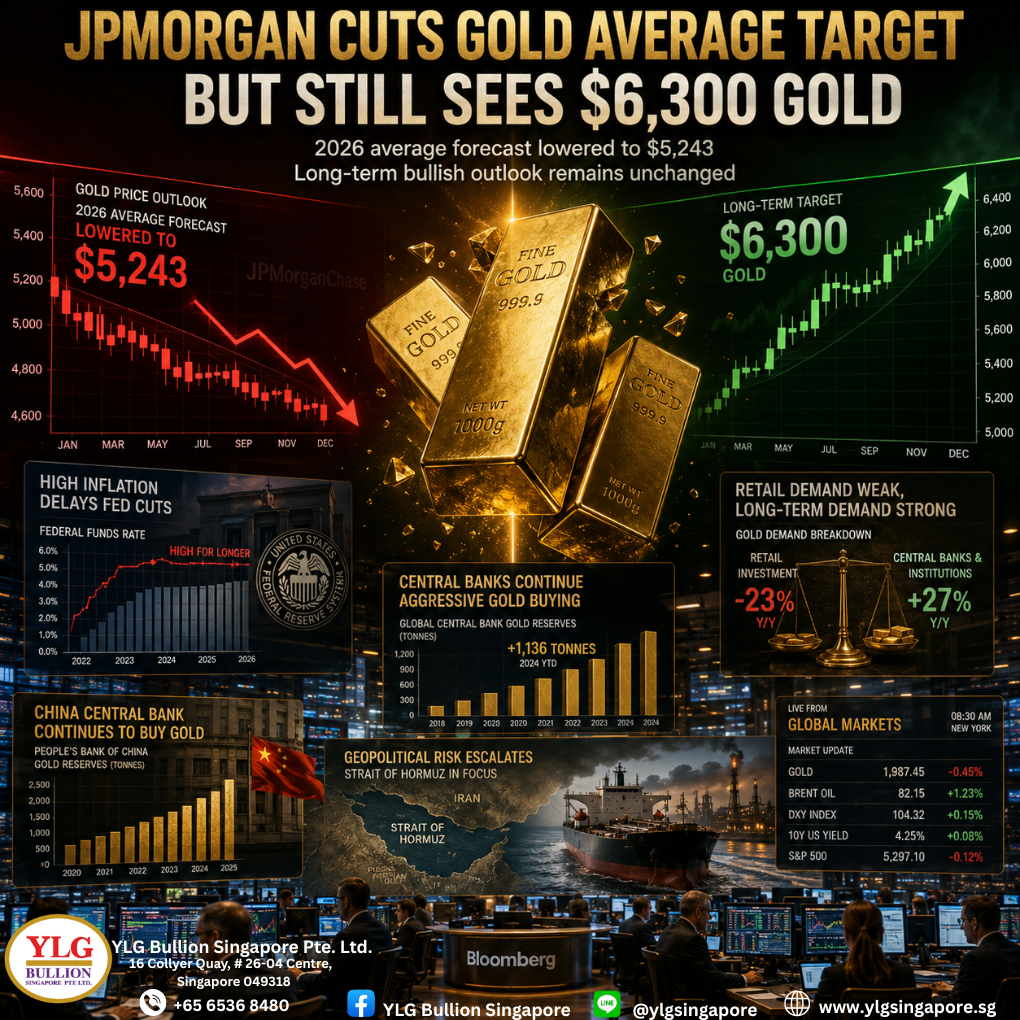

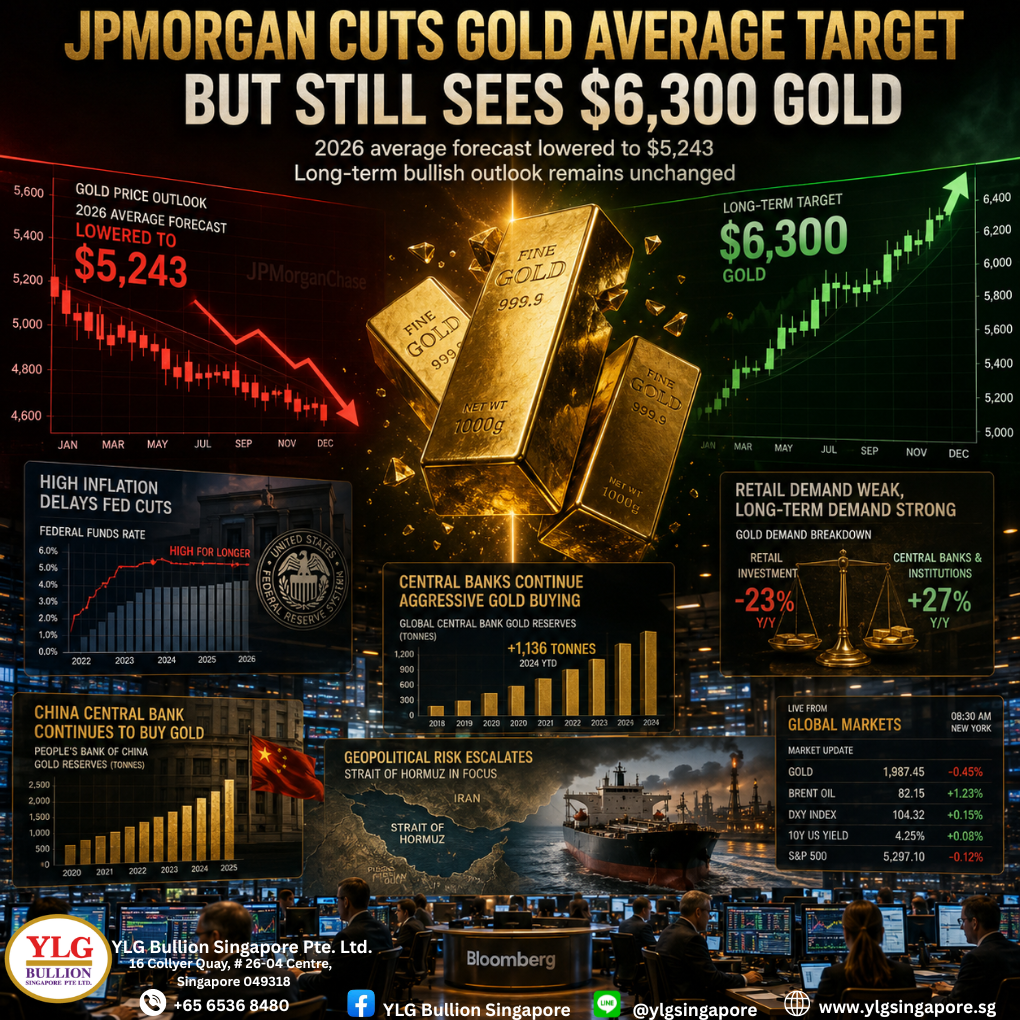

JPMorgan released a major update to its gold outlook this week, lowering its average gold price forecast for 2026 from $5,708 to $5,243 per ounce. At first glance, the move appeared surprisingly bearish.

However, despite the reduction in the annual average forecast, the bank maintained its bullish year-end target of $6,300 per ounce — signaling that JPMorgan’s broader long-term outlook for gold remains largely unchanged.

Why the Forecast Was Lowered

The key distinction lies between an “average annual price” and a “year-end target.”

The revised $5,243 forecast represents the estimated average price of gold throughout 2026, including the weaker first-half performance already seen this year. With gold recently trading near $4,540 per ounce, the lower average simply reflects current market conditions rather than a shift in long-term expectations.

Importantly, JPMorgan emphasized that its medium-term bullish outlook remains intact.

The bank expects investor demand and central bank accumulation to strengthen again during the second half of 2026 as inflation concerns and energy-related uncertainties gradually ease.

High Interest Rates Continue Pressuring Gold

Investor demand for gold has weakened considerably in recent months.

According to JPMorgan, futures market open interest and ETF inflows remain subdued as traders continue favoring bonds over non-yielding assets like gold.

One major reason is persistent inflation pressure. April CPI rose 3.8%, while PPI surged 6% — the highest level in nearly four years. These figures significantly reduced market expectations for Federal Reserve rate cuts this year.

Data from the CME FedWatch Tool also indicates that markets increasingly expect the Fed to maintain interest rates around 3.50%–3.75% throughout 2026.

As long as rates remain elevated, short-term investor appetite for gold may stay limited.

Central Banks Continue Buying Gold Aggressively

Despite softer retail investment demand, central banks continue to accumulate gold reserves at a strong pace.

Global central banks purchased a net 244 tons of gold during the first quarter of 2026 — above both the previous quarter and the five-year average.

China remains one of the strongest buyers. The People’s Bank of China has now expanded its gold reserves for 18 consecutive months. In April alone, the PBOC reportedly purchased an additional 8.1 tons of gold, far exceeding its historical monthly average.

This ongoing accumulation reflects growing long-term strategic demand among emerging-market economies.

Currently, emerging-market central banks hold an average of only 14.66% of reserves in gold, compared to approximately 31.60% among developed economies.

That gap suggests substantial room for future accumulation.

Why JPMorgan Still Expects $6,300 Gold

JPMorgan believes several factors could support a stronger gold rally during the second half of 2026.

First, geopolitical and energy-related risks may gradually stabilize. Tensions involving the United States and Iran have increased oil market volatility, but both sides also face growing economic and political pressure to avoid prolonged escalation.

If the Strait of Hormuz remains open and energy prices begin to ease, inflation pressure could moderate significantly. That scenario would potentially allow the Federal Reserve more flexibility to eventually lower interest rates.

Second, structural gold demand remains firmly supported by central bank diversification strategies and long-term reserve management.

These factors continue to provide a strong foundation for gold’s long-term outlook despite near-term volatility.

YLG Bullion Singapore Outlook

YLG Bullion Singapore continues to monitor the gold market closely amid ongoing macroeconomic uncertainty.

In the short term, key technical support remains near $4,500 per ounce. Holding above this level could allow gold to rebound toward resistance levels around $4,765–$4,890 per ounce.

While near-term price action may remain volatile, the broader long-term outlook for gold continues to be supported by persistent central bank demand, global reserve diversification, and expectations for eventual monetary policy easing.

For long-term investors, JPMorgan’s latest report highlights an important distinction: lowering an annual average forecast does not necessarily mean changing the long-term trend.

The broader bullish narrative for gold may still remain very much alive.

Related Investment Knowledge

Gold Drops Below US$4,000 for the First Time in 2026: Correction or Long-Term Opportunity

All Eyes on the First FOMC Meeting Under Kevin Warsh